Most Buy Now Pay Later products do not fail during checkout.

They fail 90 days later.

The transaction looked successful. The approval flow felt smooth. The merchant conversion rate improved. Investors liked the growth chart.

Then repayment delays started increasing. Fraud patterns became harder to detect. Chargeback handling slowed down. Regulatory reporting became chaotic. Recovery workflows stayed manual while transaction volume scaled aggressively.

That’s the hidden reality of BNPL infrastructure.

The checkout experience is only the visible layer.

The real system lives underneath, inside the credit engine, event pipelines, repayment orchestration, fraud controls, payment orchestration platform architecture and BNPL architecture operational reporting systems holding the platform together.

And this is exactly why modern BNPL platform development and fintech software development have become far more complex than adding installment options to a payment gateway.

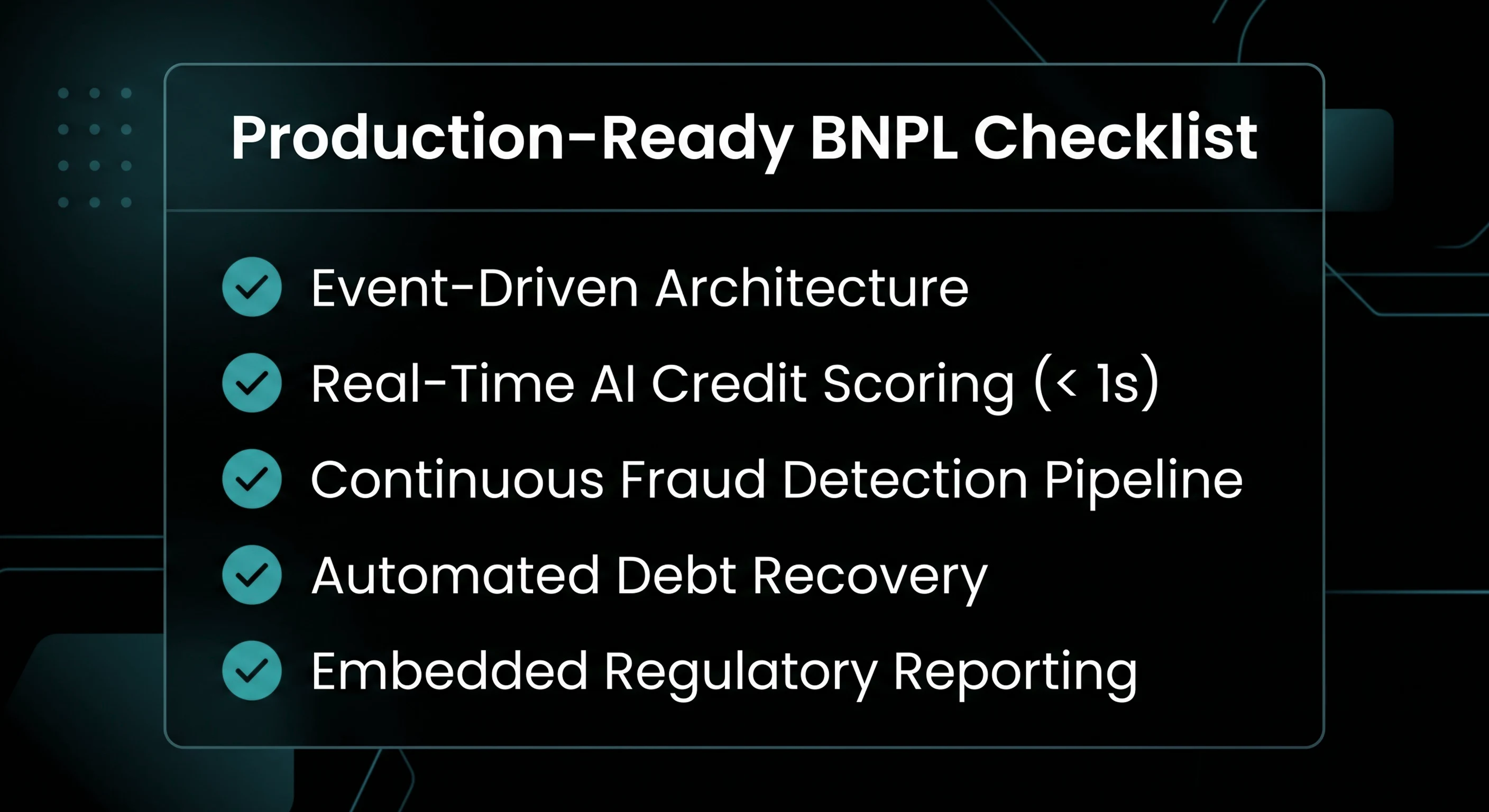

The companies surviving long-term are not simply optimizing approval speed. They are building systems capable of making real-time credit decisioning safely at enormous scale without collapsing operationally later.

$3.9TProjected global BNPL transaction volume by 2030. |

30%Average increase in merchant checkout conversion rates. |

< 1sRequired risk decision speed to prevent cart abandonment. |

A lot of founders underestimate this early.

The frontend experience feels lightweight.

Select installments, verify identity, approve transaction.

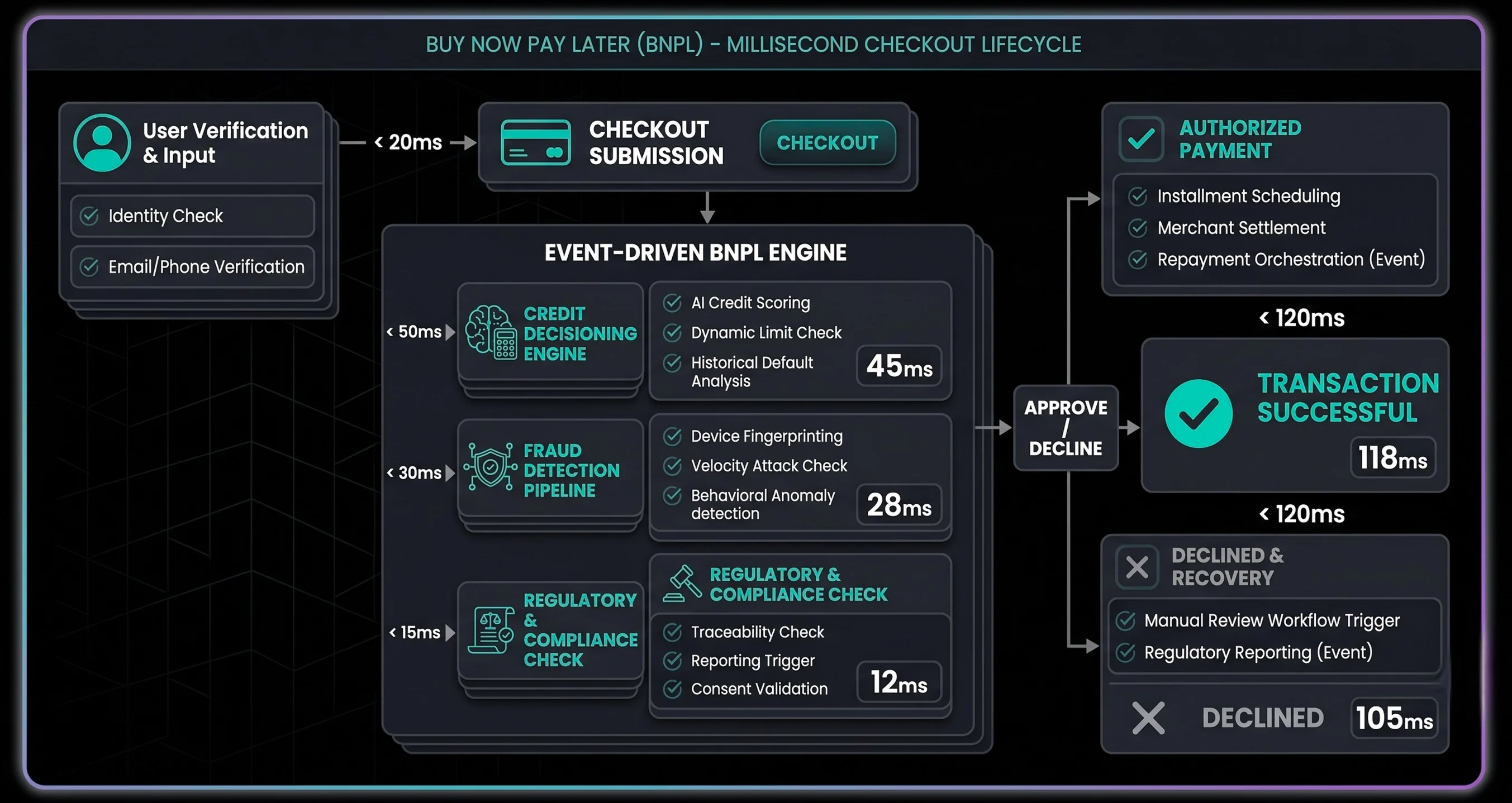

But operationally, a BNPL infrastructure platform is simultaneously handling:

All inside a few seconds during checkout.

That is why strong buy now pay later architecture and BNPL app development strategies prioritize event-driven infrastructure from the beginning. Because traditional synchronous systems struggle badly once transaction concurrency rises.

Modern BNPL systems need:

Without slowing checkout performance.

Most users never think about the infrastructure behind a BNPL decision.

They only experience approved or declined.

Which means the approval engine quietly becomes the most important part of the entire business. And in competitive checkout environments, decision speed matters massively.

"In competitive checkout environments, decision speed matters massively. A slow approval flow damages merchant conversion immediately."

A slow approval flow damages merchant conversion immediately. This is the reason behind why modern credit risk engine systems increasingly rely on event-stream processing and AI-driven scoring models instead of static underwriting rules for real-time credit decisioning.

The platform continuously evaluates transaction behavior, repayment history, merchant category, device intelligence, behavioral signals, income estimation, fintech fraud detection signals and fraud probability simultaneously.

And it needs to do this in milliseconds. Not minutes.

Why? Because checkout abandonment increases aggressively once friction enters the approval flow

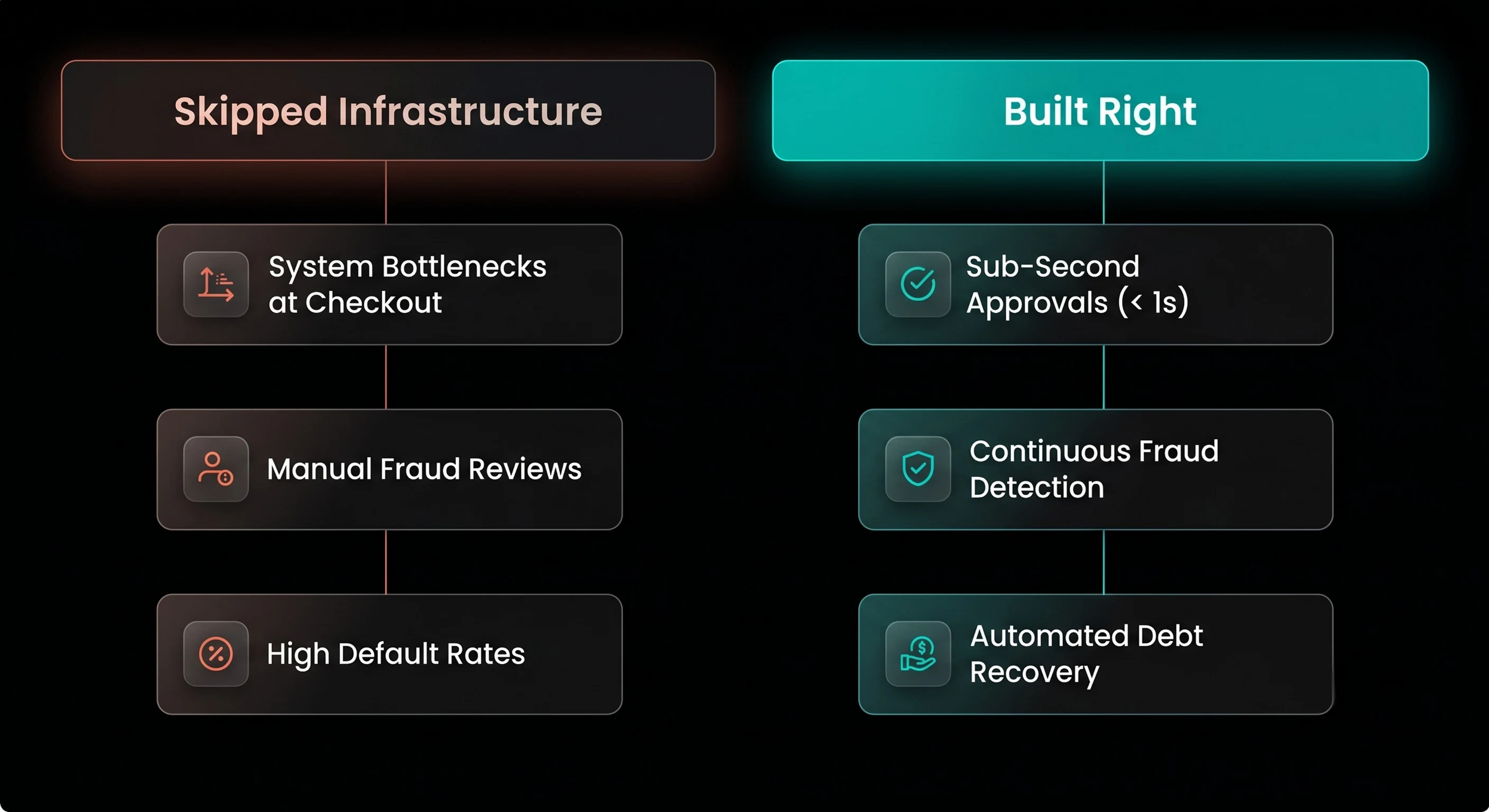

Traditional monolithic fintech systems struggle badly under BNPL concurrency pressure.

The reason is simple.

Too many operations happen simultaneously:

Trying to handle this sequentially creates bottlenecks immediately.

This is why modern automated lending systems and fintech software development teams increasingly use event-driven BNPL infrastructure powered through Kafka, RabbitMQ, AWS EventBridge or similar asynchronous infrastructure layers.

The advantage is operational elasticity.

Instead of blocking transactions while every process completes sequentially, services communicate through distributed events independently.

That creates:

And most importantly, operational resilience during transaction spikes.

A surprising number of BNPL platforms underestimate merchant integration complexity.

The easiest product to integrate usually wins merchant adoption fastest.

This is why strong scalable checkout integration design matters so much operationally.

Merchants expect:

The onboarding experience must feel simple technically. Even if the infrastructure underneath is extremely sophisticated.

Mature BNPL ecosystems and automated lending platform providers now provide:

Because reducing merchant engineering effort directly improves platform expansion speed.

This is one of the hardest operational balances in BNPL infrastructure.

Frictionless approval improves conversion. Weak risk controls increase default exposure. Strong BNPL infrastructure systems solve this through adaptive decisioning and advanced BNPL risk management strategies rather than rigid verification workflows. Low-risk transactions move through minimal friction pathways.

High-risk behavior dynamically triggers:

This is where AI-driven underwriting and AI-driven credit scoring become extremely valuable.

Instead of static approval logic, systems continuously adapt risk models using:

This creates far more flexible operational risk management compared to traditional fixed-rule systems.

One major mistake many early BNPL products make is relying too heavily on repayment history before strengthening fraud infrastructure. And that creates delayed visibility.

Modern fintech payment gateway ecosystems and automated lending platform systems increasingly integrate fraud analysis directly into transaction orchestration itself.

The system continuously evaluates:

This is done before approvals finalize.

This matters because fraud exposure compounds aggressively under high transaction concurrency. And once transaction volume scales, manual fraud review becomes operationally impossible.

"Fraud exposure compounds aggressively under high concurrency. And once transaction volume scales, manual fraud review becomes operationally impossible."

Most BNPL products focus heavily on acquisition and checkout optimization early. Very few prioritize collections architecture seriously enough. That is what becomes dangerous later. Because repayment recovery workflows become exponentially harder once scale increases.

Strong BNPL infrastructure systems automate:

Modern BNPL architecture automates recovery workflows without depending heavily on manual operations teams.

This is one of the biggest operational differences between scalable lending platforms and short-lived fintech products. The systems surviving long-term usually built repayment orchestration early. Not after default rates started becoming painful.

A lot of fintech founders still underestimate reporting complexity in lending systems.

As transaction volume grows, regulators increasingly expect:

Manually generating these reports becomes unsustainable quickly.

This is why mature regtech for startups infrastructure increasingly embeds reporting directly into event pipelines and operational data architecture itself. Every approval, repayment, fraud event and risk decision becomes part of an auditable operational stream automatically.

That dramatically reduces operational reporting chaos later. And more importantly, it prevents painful data restructuring once regulators request deeper visibility.

One of the biggest long-term risks in BNPL systems is tightly coupled infrastructure.

When credit scoring, payment processing, fraud detection and repayment systems become deeply dependent on each other operationally, future scaling becomes extremely painful. Strong BNPL platform development and BNPL app development prioritize modularity aggressively.

This allows:

This becomes extremely important once products expand internationally or introduce new financing products later.

At Seaflux, BNPL infrastructure is built as scalable lending architecture, not just lightweight checkout tooling. As a fintech software development company, the focus is on creating systems that can handle real-time lending complexity at scale.

Through fintech software development, buy now pay later software development, lending platform development, custom fintech solutions and AI development services, platforms are designed to support:

Our custom software development services and BNPL app development approach help businesses balance checkout speed with operational resilience as transaction volume grows.

Because the hardest part of BNPL systems is not approving transactions quickly. It is managing the operational complexity that follows at scale.

If your BNPL platform suddenly processed 50x more transactions next quarter, would your infrastructure still make sub-second risk decisions confidently?

Schedule a meeting with us to build scalable, AI-driven BNPL and fintech infrastructure that grows without operational instability.

Schedule a meeting →

Business Development Executive