7/10 fintech founders think compliance becomes important after scale.

And Banks think the opposite.

The moment your product starts touching regulated money movement, storing identity data, or processing transactions, your infrastructure is already being evaluated differently. Not like a startup product. Like financial infrastructure.

That shift happens earlier than most teams expect.

A payment feature launches quickly. User onboarding starts growing. APIs get stitched together fast. Product teams optimize for speed because early traction matters more than process.

Then the first serious partnership conversation begins.

Suddenly questions appear that product teams were never prepared for:

How is PII isolated?

Where are audit trails stored?

What touches cardholder data?

How are AML checks enforced operationally?

Can access history be reconstructed cleanly?

This is where weak architecture becomes expensive.

Not because regulators slow companies down.

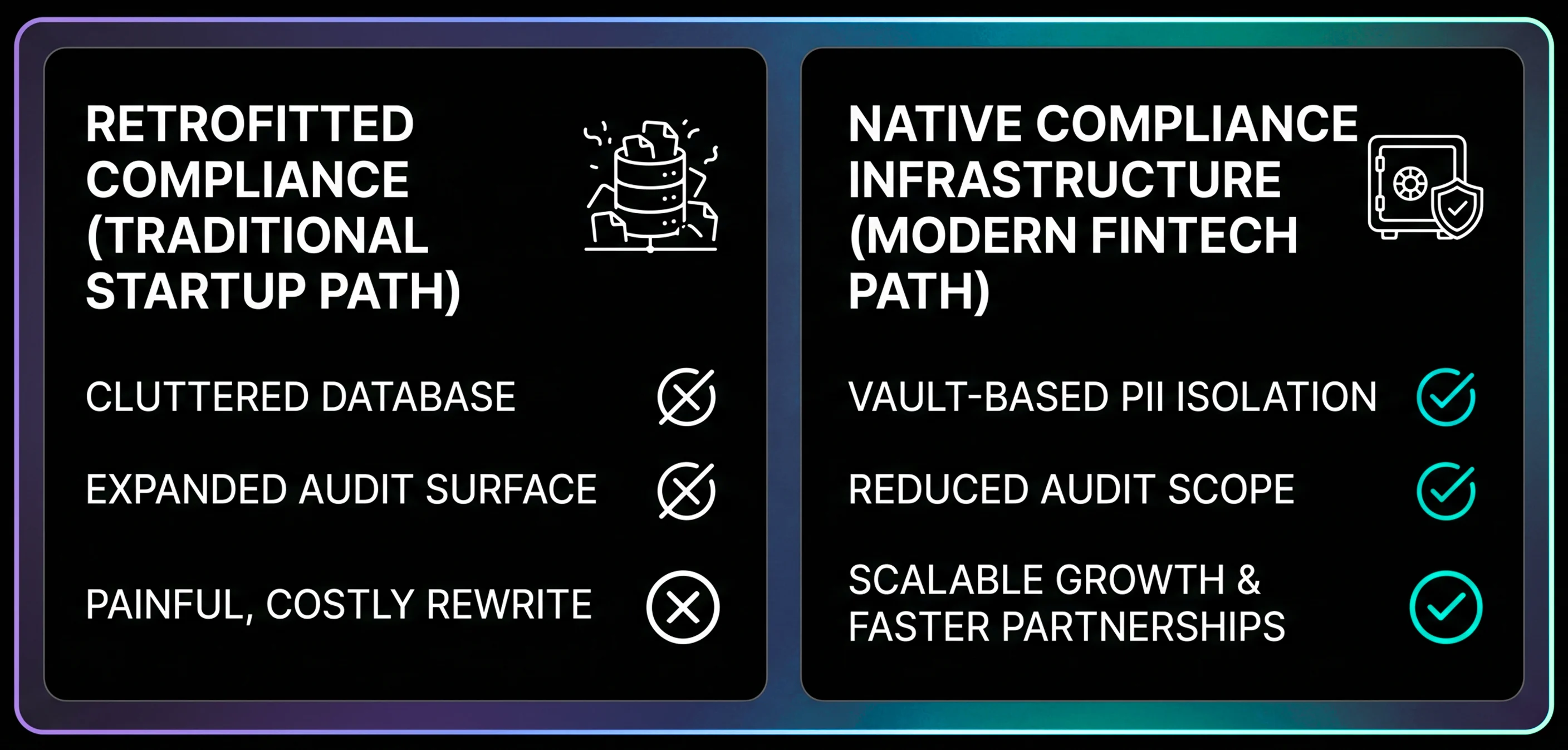

Because retrofitting fintech compliance into a live fintech system is one of the most painful infrastructure rewrites a startup can go through.

That’s why modern fintech compliance architecture and fintech regulatory compliance strategy are no longer treated as legal preparation. They’re becoming core engineering decisions from day one.

Early-stage fintech products often move fast with convenience-first architecture.

User identity data gets stored directly inside application databases. Transaction logs expose sensitive metadata. Internal services share unrestricted access to financial records because it simplifies development initially.

Nothing breaks immediately. But over time, sensitive information spreads across systems that were never designed to handle regulated data properly.

That creates two major problems:

This is exactly why mature fintech infrastructure now prioritizes PII data isolation early as part of broader fintech regulatory compliance requirements.

Instead of allowing sensitive user records to flow freely across services, modern systems increasingly isolate personally identifiable information inside dedicated vault environments with tightly controlled access layers. The advantage is not only security. It dramatically reduces future compliance complexity because once sensitive data touches fewer systems, fewer systems require deep regulatory auditing later.

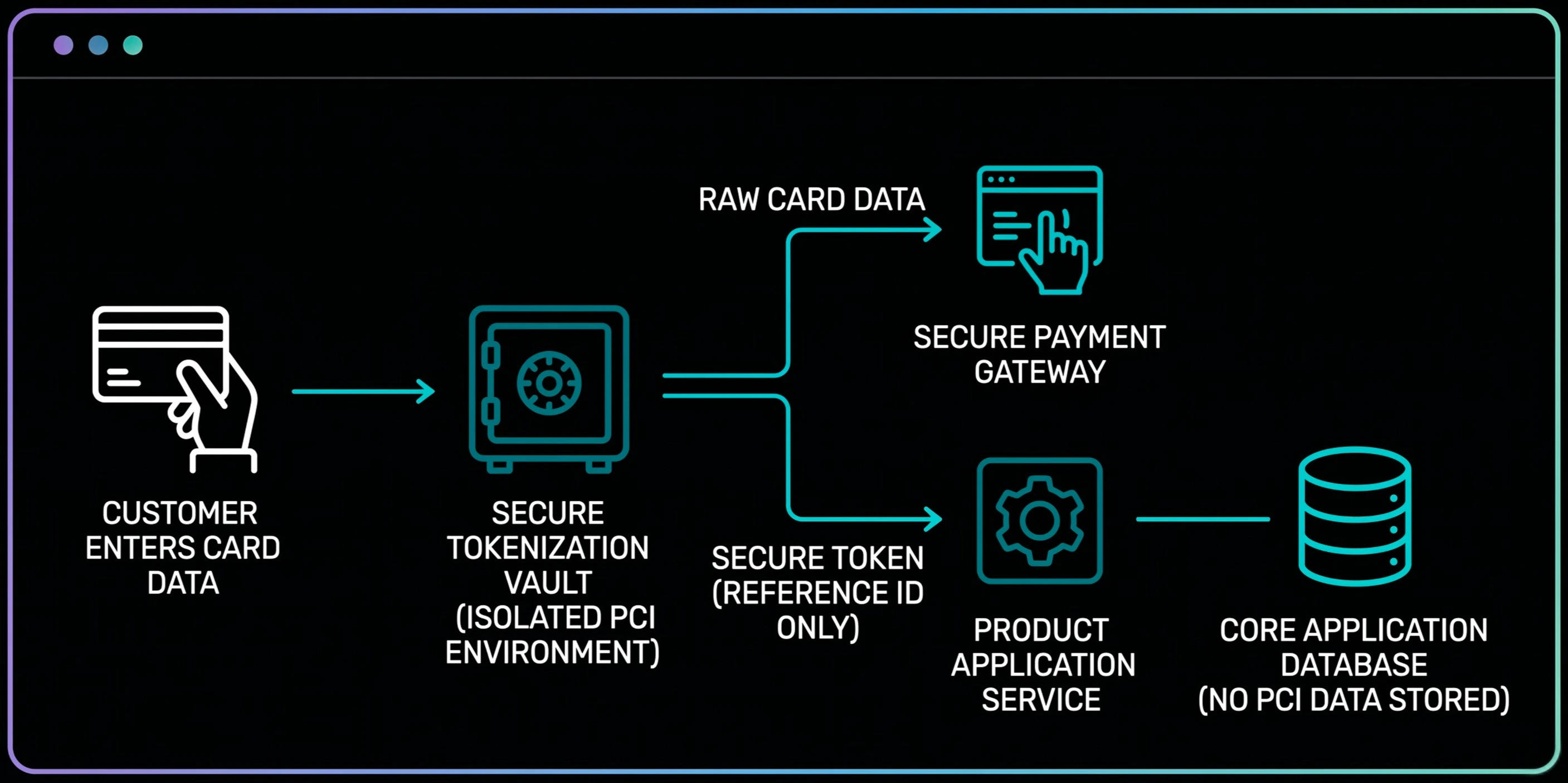

One of the biggest mistakes fintech startups make is misunderstanding PCI scope.

The problem is not storing payment data alone. The problem is how many services accidentally interact with it.

If raw cardholder information touches application services, logging systems, analytics pipelines or support tools, the compliance surface expands aggressively.

This is why PCI-DSS tokenization has become foundational in modern PCI-DSS implementation guide strategies and overall fintech compliance planning.

Rather than storing actual card information directly, systems replace sensitive financial data with secure reference tokens while the real payment data remains isolated inside hardened environments. That changes infrastructure economics significantly.

The fewer systems interacting with raw payment data:

Smart fintech systems do not try to “secure everything equally.” They reduce exposure intelligently.

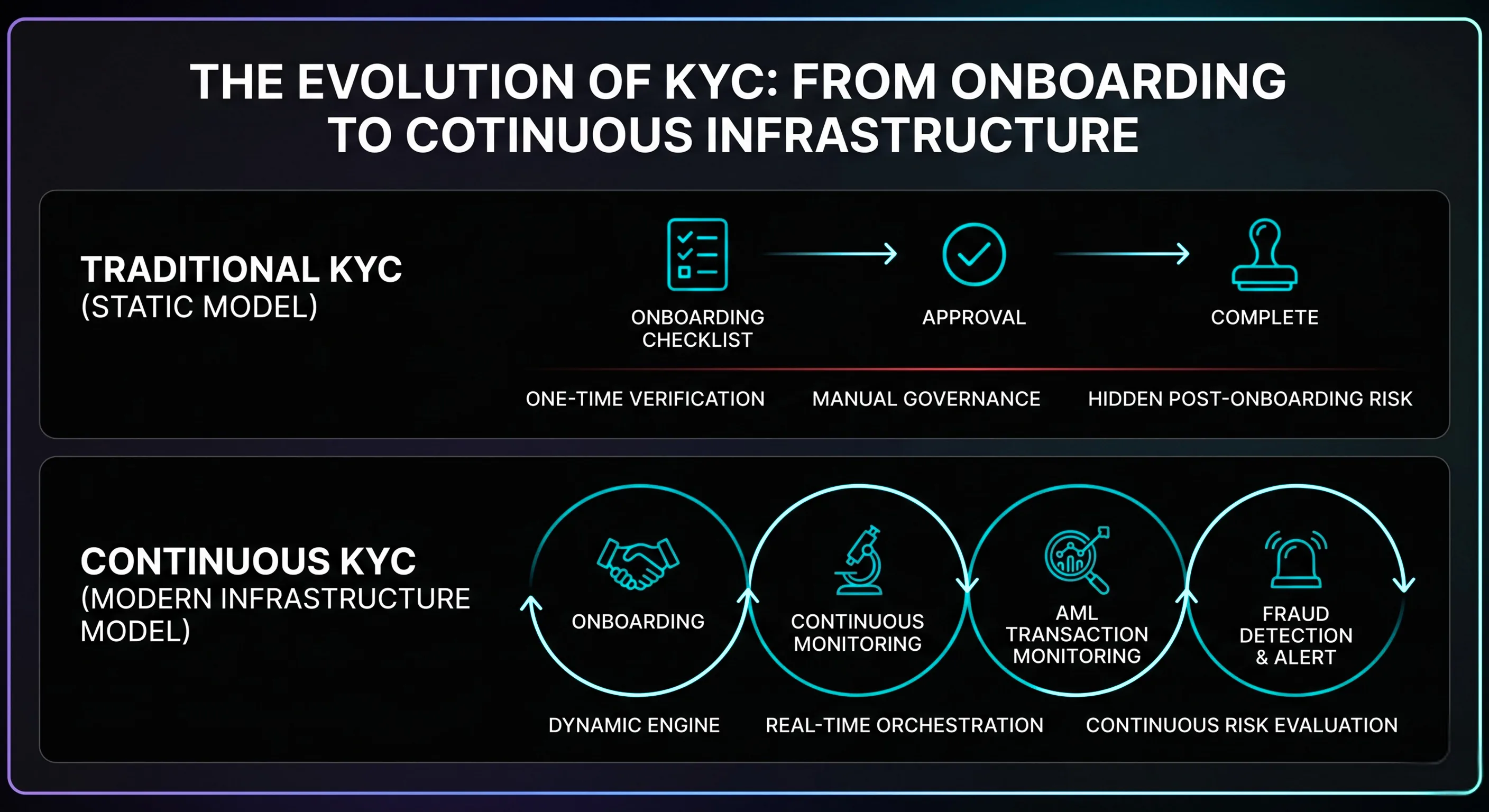

A lot of teams still think KYC AML compliance ends after account verification. That is outdated.

Modern KYC AML automation systems now function more like continuous risk engines operating across the full customer lifecycle. Fintech identity verification is only the entry point.

After onboarding, systems still need to evaluate transaction behaviour, AML transaction monitoring signals, continuous KYC monitoring requirements and suspicious activity patterns. Along with that they even need account anomalies, regional compliance triggers and growing risk signals continuously. This is where infrastructure maturity starts separating serious fintech products from temporary MVP systems.

The challenge is no longer simply approving users quickly. The challenge is maintaining scalable fintech compliance visibility without slowing operational performance.

That requires systems capable of:

Without overwhelming internal operations teams manually.

Most startups initially rely on providers like Plaid or Onfido for speed. That is usually the correct decision early. But many teams assume third-party APIs solve compliance architecture entirely. They do not.

These providers help with identity verification workflows. They do not solve:

This becomes increasingly important once products expand across markets or onboarding complexity grows.

Strong scalable KYC AML compliance workflow systems usually grow toward KYC orchestration and orchestration-based architecture. Here, multiple verification providers operate under centralized internal compliance control. That flexibility matters because no single vendor handles every jurisdiction or fraud pattern or onboarding scenario equally well under evolving fintech regulatory compliance standards.

The API is only one component. The orchestration layer becomes the real infrastructure.

One of the biggest shifts happening inside modern fintech engineering is automated compliance enforcement.

Traditional compliance depended heavily on policies written in documents and manually enforced by teams. Modern fintech systems increasingly embed compliance directly into infrastructure behavior itself. And this is where “compliance-as-code” becomes operationally powerful.

Instead of relying on manual reviews:

This dramatically reduces operational inconsistency.

More importantly, it prevents human shortcuts from quietly weakening regulated systems under scale pressure. It is because manual governance breaks quickly once transaction volume increases.

Infrastructure-driven enforcement scales much more reliably.

One of the biggest infrastructure upgrades happening across fintech systems is confidential computing and secure enclave architecture.

Sensitive operations now run inside isolated environments instead of traditional shared compute systems. AWS Nitro Enclaves help protect critical workloads and sensitive processing operations. Azure Confidential Computing also strengthens infrastructure security and private data protection.

This matters particularly for:

The reason is simple.

Even if broader infrastructure environments face compromise, isolated enclaves dramatically reduce exposure risk around highly sensitive operations.

This is becoming increasingly important as fintech platforms scale into enterprise partnerships and regulated financial ecosystems where infrastructure trust and fintech regulatory compliance readiness matter operationally.

Modern financial data encryption standards are no longer limited to encrypting databases. They now focus heavily on isolating execution environments themselves.

Fintech systems are increasingly expected to explain operational history clearly.

Not just to regulators. But to banking partners, enterprise clients, auditors and security teams.

Questions become operational very quickly:

Who accessed this account?

When was this transaction approved?

What changed during onboarding review?

Can event history be reconstructed accurately?

This is why immutable audit systems are becoming core fintech compliance architecture.

Instead of editable operational records, modern platforms increasingly rely on append-only event structures, immutable audit logs, and tamper-resistant audit pipelines that preserve historical activity continuously for stronger fintech regulatory compliance and operational defensibility.

This protects:

And once enterprise partnerships begin, this operational visibility becomes incredibly important.

Most founders think weak compliance creates legal problems eventually.

The bigger problem is operational slowdown.

Because once infrastructure maturity falls behind growth:

This is why regtech for startups is increasingly shifting toward infrastructure-first thinking instead of documentation-heavy compliance management later.

The fastest-moving fintech companies today are not ignoring compliance. But they are building systems where security, auditability and data isolation already exist operationally before scale arrives. That is what allows product velocity to continue later without painful backend rewrites.

At Seaflux, infrastructure is built around operational trust from day one instead of retrofitted compliance later. As a fintech software development company and custom software development company, Seaflux delivers custom fintech solutions designed for scalable, regulation-ready growth.

Through fintech software development, cloud security & compliance, API integration, data engineering, and AI-driven infrastructure, systems are architected to support:

As a fintech compliance consulting and AI development services provider, Seaflux helps fintech platforms scale securely without operational or compliance bottlenecks.

Schedule a meeting with us to build compliant, scalable fintech infrastructure from the start.

Business Development Executive